8 May 2026

Series: MSc student research contributions to thought leadership

This thought leadership article is part of a series written by recent University of Edinburgh Business School graduates. Each piece distils the author’s MSc dissertation, which involves independent research and in-depth analysis. Together, these articles showcase some of the strongest student research from our MSc Climate Change Finance and Investment programme.

While corporations face escalating pressure to decarbonise, the financial impact of setting ambitious climate targets is uncertain. This research examines financial returns on Science-Based Targets (SBTs), showing when, where, for whom, and how these specific, credible commitments translate into financial performance.

The challenge: the contested payoff of Science-Based Targets

The financial return on a Science-Based Target (SBT) isn’t a given; a firm’s structure (public vs. private), strategy (target ambition), and stability (financial leverage) determine the outcome. While corporations face escalating pressure to decarbonise, the financial impact of setting ambitious climate targets is uncertain. The literature is divided, with some studies finding a “win-win” and others a “costly commitment.”

My research resolves this conflict by focusing on the Science-Based Targets initiative (SBTi). The findings show that the search for a universal “business case” is the wrong question. Instead, the research reveals a more nuanced reality, showing when, where, for whom, and how these specific, credible commitments translate into financial performance.

Data and method

I assembled a panel of 4,000+ firms, public and private, linking detailed SBTi records to financials. A firm- and time-fixed-effects framework was used to isolate the impact of SBT validation from stable, unobserved characteristics (e.g., culture, brand, managerial quality). This design focuses on the shift that occurs when promises become implementation.

Findings: a contingent framework for financial impact

My analysis shows that the financial consequences of adopting SBTs are not uniform. They depend critically on the timing of validation, the firm’s ownership, its strategic ambition, and its capital structure.

Finding 1: two-stage reality

Promise rewarded, execution costly. The financial impact of an SBT is in two distinct stages. An initial public commitment earns positive financial signals. An “implementation dip”—a statistically significant decline in core operating profitability—later outweighs these early benefits after the target is officially validated. This is the moment strategic promises become real, and costly, operational changes.

Finding 2: public–private chasm

Public firms absorb the shock, private firms are insulated. Firms do not bear implementation costs equally. There is a stark “Public-Private Chasm,” where negative financial impacts concentrate almost exclusively in publicly-listed firms. Private firms, which face less quarterly earnings pressure, show no statistically significant decline in performance.

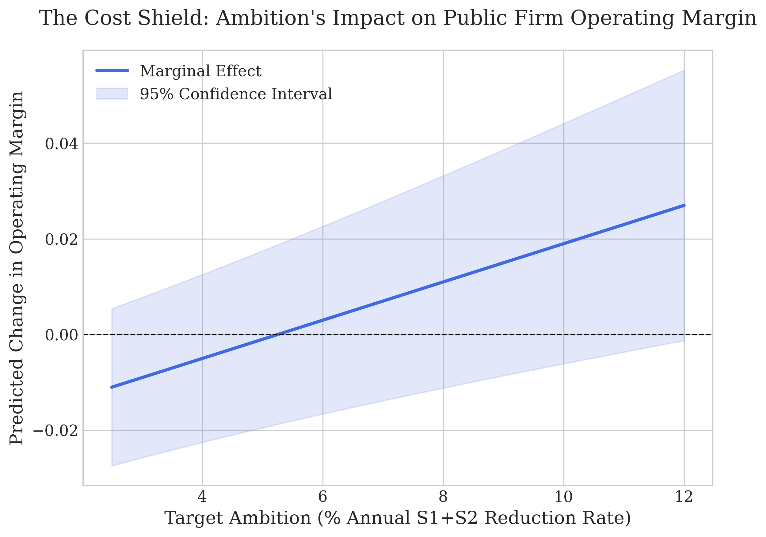

Finding 3: ambition shield

Boldness buffers the bottom line. While public firms bear the costs, their strategic choices powerfully mitigate the impact. The analysis reveals the “Ambition Shield”: a direct effect where higher target ambition significantly reduces the negative financial shock of validation. As Figure 1 shows, setting more aggressive targets forces firms to pursue greater operational efficiencies and innovations that ultimately protect their bottom line.

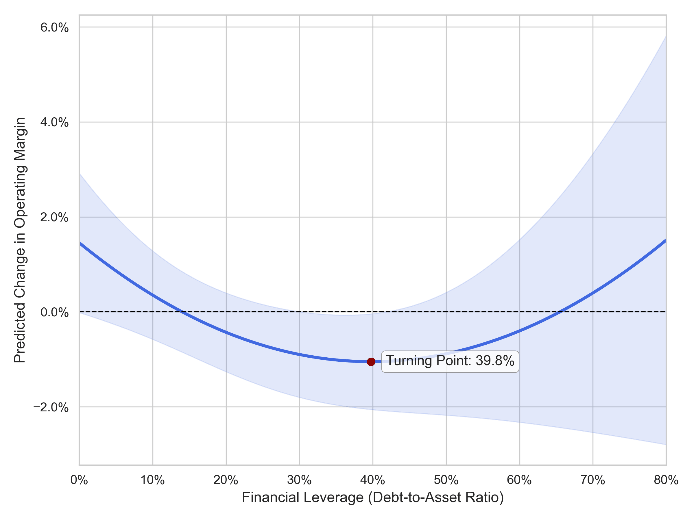

Finding 4: leverage trap

High debt deepens the dip. A firm’s pre-existing financial health dictates its ability to navigate the transition. The analysis uncovers the non-linear “Leverage Trap.” As Figure 2 shows, the negative financial impact of validation proves most severe for public firms with moderate-to-high levels of debt, which struggle to fund the necessary long-term investments.

Finding 5: market indifference

Deep operational shifts, muted market response. Despite these internal shifts, the research shows a consistent “market indifference.” SBT validation has no statistically significant average impact on headline profitability (Return on Assets) or market valuation (Tobin’s Q). The story of SBTs reveals an internal operational realignment, not an immediate market reward or penalty.

| Finding | Description |

|---|---|

| Two-Stage Reality | Firms first see positive financial signals after a commitment, followed by tangible operational costs after target validation. |

| Public-Private Chasm | Publicly-listed firms almost exclusively bear the operational costs of validation; private firms show no significant average impact. |

| Ambition Shield | For public firms, higher target ambition acts as a powerful cost shield, significantly mitigating the negative financial impact on operational performance. |

| Leverage Trap | A firm’s capital structure has a non-linear effect; the negative financial shock proves most severe for firms with moderate-to-high levels of debt. |

| Market Indifference | Significant operational shifts do not translate into a discernible average impact on headline profitability (ROA) or market valuation (Tobin’s Q). |

The bottom line

Science-based targets create near-term operating costs, especially for public and leveraged firms, but ambition and balance-sheet strength can neutralise much of the dip. The pay-off is contingent—and managerial choices determine which side of that contingency a firm lands on.

Implications for decision-makers

- Build (don’t assume) the business case. Pair high ambition with sound balance sheets; low ambition + higher leverage risks value destruction.

- Communicate the inside game. If markets are indifferent, firms should translate operational progress into credible, decision-useful disclosures. Investors need tools that go beyond ESG headlines.

- Align climate and corporate finance. Many firms need a financial transition (de-leveraging, long-term capital) to enable an operational transition.

Tanner Looney

Tanner is a recent graduate from the MSc Climate Change Finance and Investment at the University of Edinburgh Business School. He is now a Finance and Mergers & Acquisitions Analyst at Masdar (UK), overseeing deals including offshore wind in the UK, and Battery Energy Storage Systems in the UK and Europe.